Double-entry bookkeeping revolutionised business by introducing a self-checking system of financial integrity. In the world of software, Behaviour-Driven Development (BDD) does something strikingly similar — pairing each feature with a clear, testable description of how it should behave. Double-entry bookkeeping and automated software testing might seem worlds apart – one emerged in Renaissance-era accounting and the other in modern software development. Yet conceptually, they serve a similar purpose: both introduce systems of checks and balances to ensure integrity and accuracy in their respective domains. In accounting, double-entry bookkeeping requires every transaction to be recorded in two accounts (debits and credits) that must balance, creating an internal self-checking mechanism. In software, automated tests act as a parallel record of expected behaviour, continuously verifying that the code produces the intended outcomes. This post explores how a 500-year-old accounting innovation revolutionised financial record-keeping and how its spirit lives on in the way we write and test software today.

Double-Entry Bookkeeping: A Revolution in Accounting

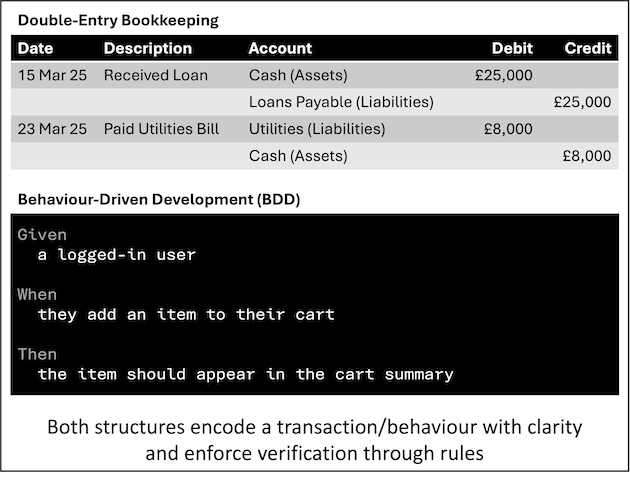

Double-entry bookkeeping, formalised in the late 15th century, forever changed how businesses track money. Prior to its adoption, many merchants used simple single-entry records – essentially just running diaries of income and expenses. This often proved error-prone and made it hard to get a clear financial picture. The double-entry system introduced the idea that every transaction is recorded twice: once as a debit in one account and once as a credit in another. These dual entries must always sum to zero, meaning the books “balance” – a built-in check that flags mistakes if the debits and credits don’t match.

In 1494, the mathematician Luca Pacioli published the first detailed description of double-entry accounting in his book Summa de Arithmetica. Although he didn’t invent it (Italian merchants were already using it), Pacioli’s work codified and spread this technique across Europe. Historians note that this was nothing short of a revolution in business. Suddenly, merchants could see a comprehensive view of their finances “in neat little rows,” tracking not just cash on hand but also inventory, debts, and profits for each area of their business.

Why was this such a game-changer? For one, double-entry bookkeeping acts as an internal control mechanism against errors and fraud. Because every transaction affects two accounts, a mistake or omission is easier to spot – the books simply won’t reconcile if something is off. It also creates an audit trail: by reviewing the two entries for each transaction, auditors can trace and verify business activities with confidence. Over time, double-entry became the bedrock of modern accounting systems, instilling trust in financial statements and enabling more complex enterprises.

Automated Testing in Software Development: A Modern Safety Net

Fast forward to the present, and software engineers face their own accuracy challenges. Writing complex code by itself is not enough — we need ways to ensure the code behaves as intended and continues to do so as it evolves. That’s where automated testing comes in.

More specifically, many teams use Behaviour-Driven Development (BDD) — an approach that structures tests around expected behaviours, written in a clear, human-readable format. Instead of merely verifying the technical outputs of functions, BDD scenarios describe what the system should do from the perspective of the user or the business.

For example, a BDD scenario in Gherkin might say:

Given a logged-in user

When they add an item to their cart

Then the item should appear in the cart summary

This is the software equivalent of a well-annotated ledger entry: it not only records what happened, but why, in language stakeholders understand. Just as double-entry bookkeeping includes context (e.g. “Paid invoice #123 for supplier X”), BDD ties system behaviour to business intent in a way that’s verifiable and collaborative.

Double-Entry Software Development

The Common Element: Dual Record Keeping

Accountants record each transaction in two places (debit and credit accounts) that must balance. Likewise, BDD encourages developers to write both the feature and its test scenario. For every feature added to the system, there’s a parallel behaviour specification — a testable record of what the system should do. The code defines the functionality; the BDD scenarios define the expected outcomes. When all BDD tests pass, it’s like the books balancing: the observed behaviour matches the declared intent. Both must agree for the system to be considered correct.

Benefits of Rigorous Double-Recording Systems

Both double-entry bookkeeping and BDD-style automated testing introduce effort, but repay it in quality and reliability. The table summarises the benefits.

| Benefit | Double-Entry Bookkeeping | Behaviour-Driven Development (BDD) |

|---|---|---|

| Human-Readable Context | Annotated transactions | Gherkin scenarios |

| Shared Understanding | Interpretable by finance teams | Interpretable by business, QA, devs |

| Built-in Verification | Ledgers must balance | Tests must pass |

| Triggers Error Detection | Mismatched entries | Failing scenarios |

| Increased Confidence | Trust the numbers | Trust software behaviour |

| Auditability | Trail of transactions | Record of desired behaviour |

| Scalability and Resilience | Allow large teams to work together safely | Allow large teams to work together safely |

Human-Readable Context: BDD uses domain-specific, plain-English syntax to describe desired behaviours. This aligns with how double-entry records are annotated and explainable to non-accountants — ensuring everyone can interpret them.

Shared Understanding: A unique benefit of BDD is that it encourages collaboration before implementation. Business analysts, developers, and testers discuss and agree on scenarios before any code is written. This mirrors how accounting frameworks provide a shared understanding between departments about what constitutes valid financial activity (Evans, 2004).

Built-in Verification: Both double-entry bookkeeping and BDD-style automated testing introduce checks and balances through redundancy. In double-entry, every financial transaction is mirrored by a complementary entry, and the two must agree. In BDD, every piece of logic is paired with a human-readable specification and a test that validates the outcome. BDD scenarios then become a safety net (catching regressions), documentation (describing behaviours), and a communication bridge (ensuring everyone understands what’s expected). In other words, BDD doesn’t just verify correctness — it aligns understanding across roles. That’s a powerful echo of how double-entry accounting brought structure, clarity, and shared trust to the messy world of money. Both systems verify data by design. Double-entry ensures every dollar is accounted for; BDD ensures that every user behaviour is anticipated and verifiable.

Triggers for Error Detection: The main benefit is that, in both cases, errors are surfaced immediately. In accounting, the books won’t balance if a transaction is mis-recorded. In software, a failing BDD scenario flags issues as soon as they arise — often before the feature even ships.

Increased Confidence: When the ledger balances, an accountant can trust the numbers. Accountants and auditors rely on balanced books to make informed decisions. When all BDD tests pass, a team can trust the software’s behaviour. Developers rely on green tests to refactor or expand codebases with confidence. In both cases, built-in verification leads to built-in confidence.

Auditability: Double-entry leaves a trail of transactions. BDD scenarios document how the system should behave, and why, so it becomes obvious when a change breaks the system. Both serve as transparent records that newcomers or reviewers can follow.

Scalability and Resilience: As businesses or software systems grow, having a reliable structure for checking accuracy becomes more important, not less. These methods scale and improve resilience under complexity. Double-entry accounting enabled large, multi-branch businesses to maintain control. BDD enables large teams to coordinate and test large software systems with clarity and alignment. When issues arise, both systems flag the problem immediately. You’re not guessing what went wrong — your structure tells you.

Costs and Challenges: Investment and Maintenance

No surprise — double-recording systems aren’t free. Understanding accounts and the logic of debits and credits takes time — just as learning how to write effective BDD scenarios requires practice and discipline. Then, once you’ve mastered the approach, double-entry still requires every transaction to be entered twice; BDD involves writing extra specifications and test code. But it doesn’t stop there. To continue gaining the benefits, ledgers need to be updated continuously and BDD scenarios need to evolve with the product. Neglect either system, and you risk false confidence or unspotted drift.

The learning curve and perceived “slowness” can be off-putting early on. Skeptics of both systems sometimes ask: “Isn’t this overkill?” Yet the cost of not having these checks — silent bugs or financial misstatements — is often far worse.

For me this is the difference between one person activity – whether finance or software development – and enterprise activity. A one person outfit can be a bit loose with discipline and get away with it. An enterprise cannot.

Why BDD not TDD?

Test-Driven Development (TDD) was the precursor to Behaviour-Driven Development (BDD). Both provide automated tests — the “double records” of the software world. So why favour BDD over TDD?

I’m a fan of TDD, but I believe BDD offers more of the benefits described above. If TDD is like balancing the books, BDD is like attaching plain-English memos to every transaction — making it easier for everyone to understand, review, and verify what’s going on.

If you want to know more about BDD then check out my section on Specification by Example.

So what about AI?

As LLMs become more integrated into development workflows, it’s worth asking whether disciplines like BDD remain relevant in an AI-assisted world.

Some argue that with the rise of Artificial Intelligence (AI), and AI code generators, there is no need for languages like Gherkin. For example, AquaQA commented on BDD is dying that “With AI and LLMs becoming increasingly adept at handling code, perhaps we’re entering a new era where behavior formulation can happen directly in code, removing the need for middleware like Gherkin.”

I disagree. AI engines can whip up code more or less instantly. But AI does not have a good reputation for whipping up quality code. Writing quality code, that doesn’t undermine the enterprise, requires discipline.

If LLMs are “friendly but helplessly untrustworthy and deeply forgetful colleagues” (Mark Ridley) then we continue to need high discipline to ensure high quality enterprise software.

Conclusion

Whether you’re managing a growing company or a complex codebase, there’s value in systems that verify themselves. Double-entry bookkeeping and Behaviour-Driven Development are more than technical tools — they are disciplines built around clarity, accountability, and confidence.

They don’t just help you catch mistakes. They let you operate with boldness. Brakes let you go faster! Both Double-entry bookkeeping and Behaviour-Driven Development’s automated tests are organisational brakes. Both practices come with a cost, but the benefits they deliver — and the risks they mitigate — make them essential for enterprise-scale reliability.

Double-entry bookkeeping revolutionised business by creating reliable records. BDD is doing the same for software by aligning code with clear, testable intent. Different eras, same core idea: two records are better than one.

References

Knight, A. (n.d.). BDD is dying. Automation Panda. Retrieved from https://automationpanda.com/2025/03/06/is-bdd-dying/

Ridley, M. (2024, 27 August). Building software with an AI team: how I built a working web app with Claude & ChatGPT. Retrieved from

https://mark-ridley.medium.com/how-i-wrote-a-working-web-app-with-chatgpt-and-claude-and-what-you-can-learn-from-it-a0cb291113de